Special Update, Week 5 - March 28, 2020

The past week provided a continuation of extremes. First, we saw the number of confirmed COVID-19 cases in the U.S. increase by a factor of 5x, hitting 131,000 and eclipsing China. Most of the growth occurred in metropolitan areas, especially New York, but the rest of the country also saw their numbers rise. Even our home state of Tennessee saw infections quadruple. Second, the nation witnessed the enactment of the most extensive government stimulus package ever ($2.2 trillion) and a record number of unemployment claims (3.3 million, the previous record was 695,000). Lastly, after experiencing the fastest drop to bear status in history, U.S. stocks took three days to gain roughly 20% before giving a chunk back on Friday.

What We Know

A range of outcomes are possible. We are a nation of approximately 330 million people. As of St. Patrick’s Day, we had roughly 4,500 confirmed cases (though the true number was likely much higher) and today we are at 140,256. Experts have different ideas about when our number of infections may peak, but until it does, we should expect a rapid increase in reported cases. We hope that the combination of shelter in place, workplace closures, and social distancing will slow the virus's progression enough to avoid overpowering of our healthcare capacity. Unfortunately, New York City has crossed the tipping point, and there is a real concern that Chicago, Detroit, New Orleans, Los Angeles, and other metropolitan areas may soon follow.

Private industry is trying to respond to shortages of materials and equipment needed to treat the ill. Resources such as life-saving ventilators are in short supply in the hardest-hit areas. In an effort to accelerate the process, on Friday the President invoked the Defense Production Act (DPA) and ordered General Motors to ramp up the production of ventilators. Other companies are retooling their assembly lines to produce a spectrum of needed supplies.

While it is clear the virus takes a higher toll on the elderly and those with comorbidity factors, the virus is impacting all age groups. The article from USA Today, Age of Coronavirus Patients in the U.S., shows hospitalizations span every age group. We’ve seen this personally in our community. The take away is that no one should discount the current health crisis.

The Federal Reserve Bank and the U.S. Government are using every tool available to combat the economic fallout of the virus. After passing the CARES Act, both houses of Congress expressed a willingness to take further action to stem the tide of the economic shutdown. The Federal Reserve is backstopping a variety of debt instruments and lending arrangements as well as acting as the buyer/lender of last resort for markets. As a result, it is unlikely their efforts will be enough to absorb the expected 15 to 30 percent drop in economic activity caused by the crisis.

Investment Implications

The extremes we’ve seen this month leaves us all reeling emotionally. The swift sell-off bred fear of losing our assets and of what could happen. The strength of this week’s sudden market rally evoked feelings of being left behind in case it was the beginning of a new bull market. Both extremes test our investment discipline.

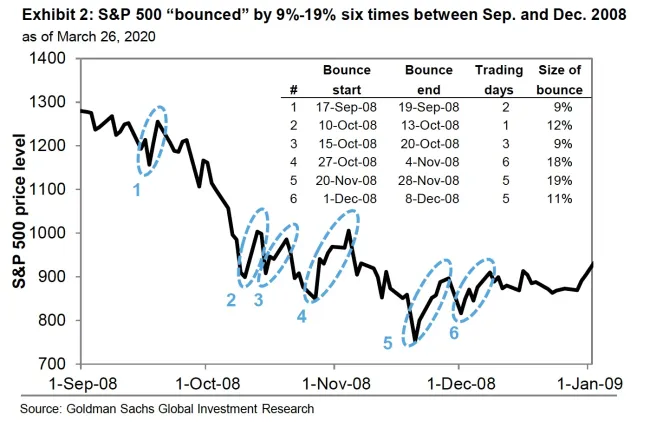

While acknowledging the possibility of a more extended move upward, historically there are many examples of sharp increases during market declines, such as those seen below in 2008.

Other examples occurred during the prolonged market turbulence in the early 1930s. There were no less than four 20% rallies before the ultimate low was reached in July of 1932. Our point is not to suggest we should expect a depression area market environment, but we are considerate of the vast majority of steep declines followed by strong rallies that do not produce new highs.

Looking Forward

While this week’s bounce has earmarks of a bear market rally, we do not know the future. After the market crossed a line in the sand, we took a small action of multiple trades as part of our planned but delayed rebalancing. From a pure asset class perspective, the most attractive valuations currently are found in international stocks, value stocks, as well as mid and small size stocks in all markets. The investment changes made this week, emphasize those areas.

Portfolio changes this week were as follows:

- 3/26/2020 Began to rebalance our Market Strategy

- This strategy utilizes a fund by DFA. The fund owns a portion of virtually all companies in the world, a total of 12,307 different companies. Unlike most popular indexes that are biased toward large companies. DFA is tilted toward lower valuation companies and small companies. Valuation disparity versus the S&P 500 index can be seen in book value. Book Value is an estimate of the value of the assets of a company. The S&P 500 index trades at 2.69 while the DFA fund trades at 1.72, representing a 36% lower valuation.

In our view, there are four key elements the markets will need to find a sustainable bottom.

- Federal Reserve intervention to stabilize and support markets

- Government stimulus

- Clarity and or improvement of the health crisis

- Investor capitulation – an absence of significant buyers in the market

All four components are somewhat relative and subjective. In our view, the first two boxes on the list have already been checked. There will likely be more action required to restart the economy, but it is clear the intention of both is to do whatever it takes. Elements three and four are yet to be seen.

Since we don’t know when news regarding the virus will begin to improve and can’t perfectly forecast investor capitulation, our plan is to continue to make measured investments as the market falls further or moves in a positive direction. These will come in the form of further "market-based" investments, as was seen this week and in the form of individual security purchases. We may also make strategic tilts or overweights if the weight of the evidence merits. We’ve outlined this strategy in more detail in previous letters which can be found on our website, http://www.cravensco.com/blog.

Summary

In looking forward, we expect challenges to lie ahead. From an investment standpoint, they will likely be stressful. As history has shown us many times before, these periods of stress and uncertainty will pass and be looked back upon as an opportunity. We plan to keep that lesson in mind as we strive to advise and make prudent investments for you.

We hope the detail we are sharing provides some confidence and understanding of our reasoning in adjusting our strategy`. Please let us know if you find this information helpful or if you have questions or concerns. Also, if you think someone else may find these communications helpful, please feel free to forward or share these letters.

If the COVID-19 situation continues to worsen (unfortunately, we expect it will), we are concerned for your health, as any friend would be. We hope you will take care to reduce your potential exposure to the virus. If you have thoughts or questions about any of the information we've shared, or on any other subject, please don't hesitate to call us. We are grateful you allow us to serve you and your family, and we will continue to make every effort to justify the trust you've bestowed on us.

Sincerely,

Your CCA Investment Team

Advisory services offered through Cravens & Company Advisors, LLC, an SEC Registered Investment Advisory Company. Securities offered through and advisory services may also be offered through FSC Securities Corporation, an Independent Registered Broker/Dealer. Member FINRA/SIPC. Not affiliated with Cravens & Company Advisors, LLC.

Investing involves risk, including the potential loss of principal. Investing involves risk, including the possible loss of principal. International investing involves additional risks, including risks associated with foreign currency, limited liquidity, government regulation, and the possibility of substantial volatility due to adverse political, economic, and other developments. The two main risks associated with fixed income investing are interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risks refer to the

possibility that the issuer of the bond will not be able to make principal and interest payments. Investments in commodities may entail significant risks and can be significantly affected by events such as variations in the commodities markets, weather, disease, embargoes, international, political, and economic developments, the success of exploration projects, tax, and other government regulations, as well as other factors. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance is no guarantee of future results. Please note that individual situations can vary. Therefore, the information presented here should only be relied upon when coordinated with personalized professional advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors alone and do not necessarily reflect the views of FSC Securities Corporation. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product.